SaaS is dead. Or at least, that’s the narrative floating around from VCs, industry leaders, and even Satya Nadella himself. And when the CEO of a $3 trillion company says something, there must be some merit to the statement

As someone who has sat on both sides of the tables, I see a more nuanced reality unfolding and it doesn’t take a genius to guess that AI has been mongering over our heads to transform SaaS as we knew it, yesterday a year or a decade back. And AI’s influence is extending far beyond traditional software budgets—it’s now making inroads into labor spend, fundamentally reshaping how businesses allocate resources. Current Market Dynamics

Venture funding to U.S. companies totaled $178 billion — gobbling up 57% of global capital. The Bay Area absorbed $90 billion of this – a 50% jump from 2023, thanks to the boom from AI investing.

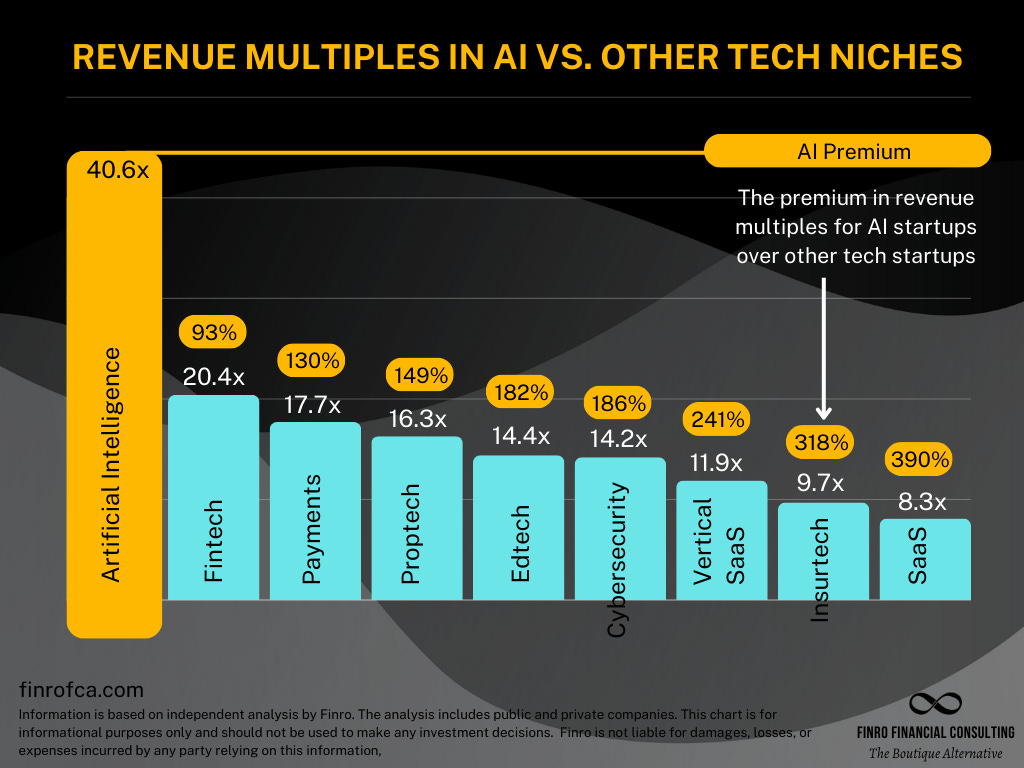

As per crunchbase, funding to AI-related companies crossed $100 billion. That’s an 80% YoY surge from $55.6 billion in 2023. Investor confidence is evident in the numbers as AI SaaS startups are commanding revenue multiples of 37.5x, significantly higher than the average SaaS multiple of 7.6x (finrofca). The speed at which AI is scaling makes every other wave of innovation look slow.

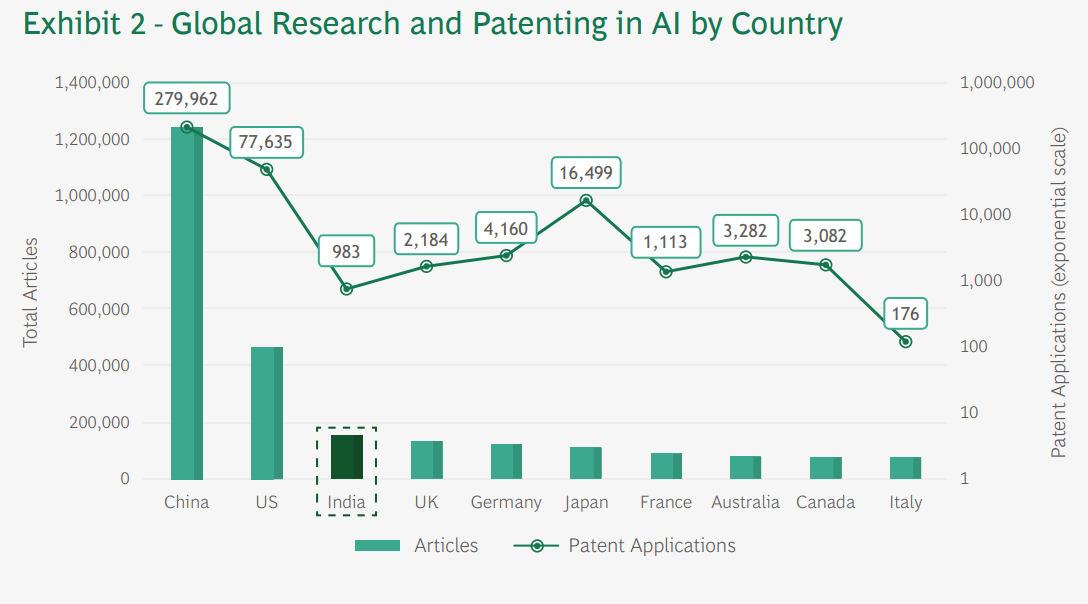

Much of this momentum comes down to R&D investment. It’s no coincidence that China, the U.S., and Japan—home to the highest concentration of AI patent applications – are also leading the charge in developing the most advanced foundational models.

Where’s the Money Moving?

-

Seed Stage – AI companies are raising rounds 28% higher than non AI startups

Nearly 3 in 4 AI deals (74%) were early-stage in 2024. AI startups raising seed rounds are seeing median rounds of $1.6 million – that’s 28% higher than non-AI startups, who’re pulling in about $1.25 million.

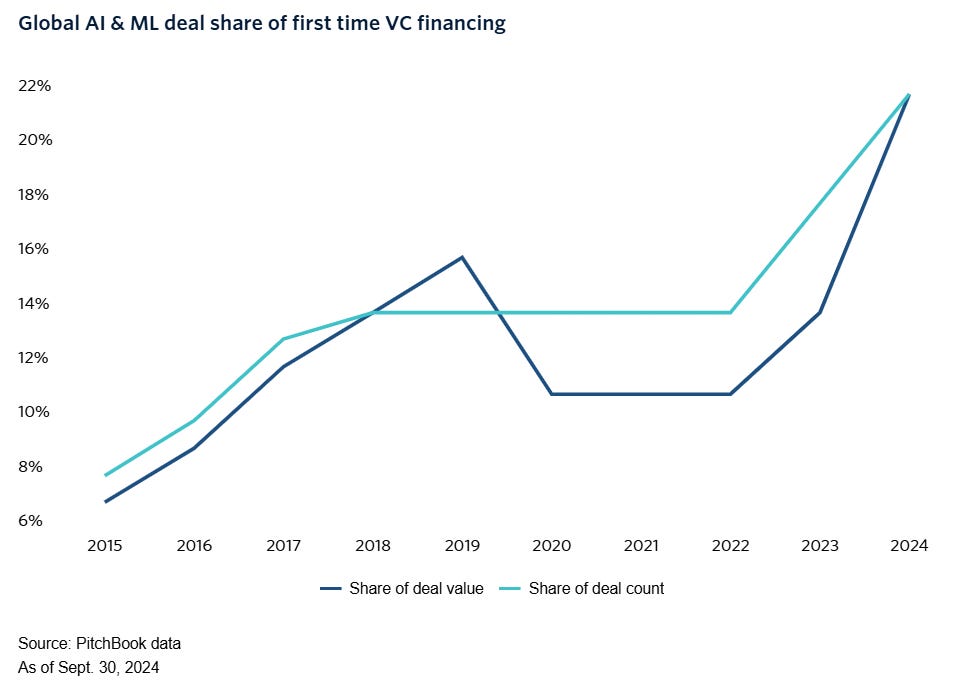

AI startups made up 22% or $7 billion of first-time VC financing. Just two years ago, that number was half.

Source: Pitchbook

The barrier to entry for AI has lowered, thanks to accessible cloud resources, open-source models and fine-tuning APIs. The real differentiator at this point is deep technical defensibility and teams’ ability to solve hard enterprise problems, not just layering AI on existing workflows.

-

Series A & B median valuations are 2.5x higher

The median AI pre-money valuations of Series A and Series B are $34.0M and $150.0M valuation, respectively. AI startups in these rounds are seeing median valuations 2.5x higher than in traditional SaaS.

Why? Because If you’ve made it to Series A/B, investors are now betting on you to achieve hyperscale adoption. But not all will make it. The adoption cycles in enterprise AI are brutal, and many of these companies are realizing that just because the tech is promising doesn’t mean it fits into existing workflows. Some will break through. Many won’t.

-

Growth Stage (Series C & Beyond) demands proprietary infrastructure

This is where the pressure is mounting. The biggest AI bets of 2024 include Databricks ($10B round), OpenAI ($6.6B), xAI ($6B), and Anthropic ($4B). These late-stage rounds are dominated by hyperscalers and sovereign wealth funds, signaling that true differentiation now demands proprietary infrastructure, not just incremental improvements.

The capital is there, but so are sky-high expectations. The ones solving real problems will raise massive rounds. The rest? They’ll burn out just as fast as they took off.

Source: finrofca

How different industries are adopting

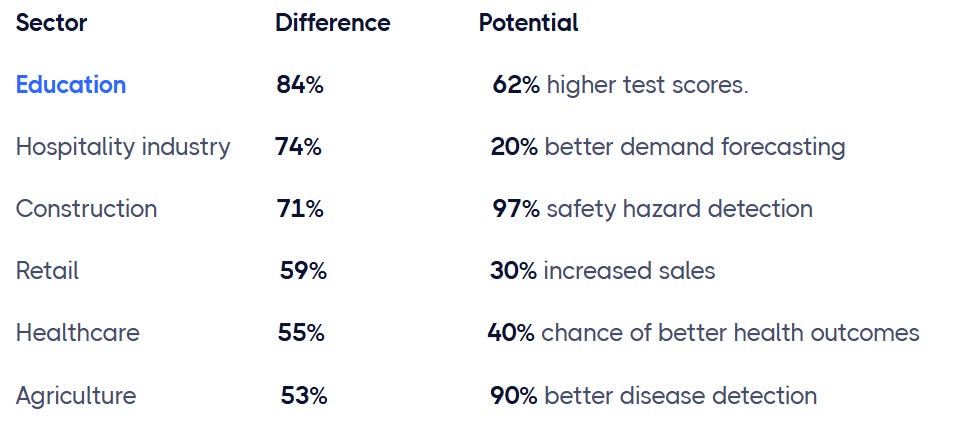

AI funding across industries is directly proportional to the substantial data volumes, potential for automation and the complexity of existing operational workflows. An Accenture report shows the profit potential in these industries after implementing AI integrations.

Source: Springsapps

-

Healthcare & Life Sciences: AI is revolutionizing drug discovery, diagnostics, and clinical workflows. Currently, 79% of healthcare organizations have adopted AI technology; $3.20 is made for every $1 invested. AI is moving from experimental technology to core infrastructure in medical delivery.

-

Finance: From fraud detection to automated underwriting and trading algorithms, generative AI alone could contribute $200–340 billion annually to global banking, primarily through productivity gains.

-

Manufacturing & Supply Chain: AI-driven predictive maintenance, logistics optimization, and robotics are redefining efficiency, reducing downtime, and streamlining operations.

Market Correction in Full Swing

Low-hanging fruits like customer service, automation, and sales are now dime a dozen. AI in developer tools has been commoditized. And when tech gets cheaper, returns shrink, investors pull back, and the price tags start correcting themselves. Incumbents will take the advantage, evident in 384 AI acquisitions in 2024, nearly matching 2023’s 397.

The AI gold rush isn’t over, but the market’s getting a reality check. Unsustainable burn, superficial value propositions, and the incumbent disadvantage are driving this consolidation.

It’s Back to the Fundamentals

At the end of the day, funding metrics and exit multiples make for good headlines, but they’re not the whole story. The enduring companies will be built by teams who understand that AI isn’t just a technical challenge – it’s a transformation challenge. Whether you’re writing checks or cashing them, it’s time to wear the operator’s hat and get back to the basics. Which ones, will make it? Here’s a framework that will help evaluate that: AI Startups: does your idea have hype, hope, or is it a hard pass